Digital Transformation

in Oil & Gas:

The Engineering Behind

the 6 Trends Defining 2026

Digital Transformation in Oil & Gas: 6 Trends Every CTO Should Prioritise in 2026

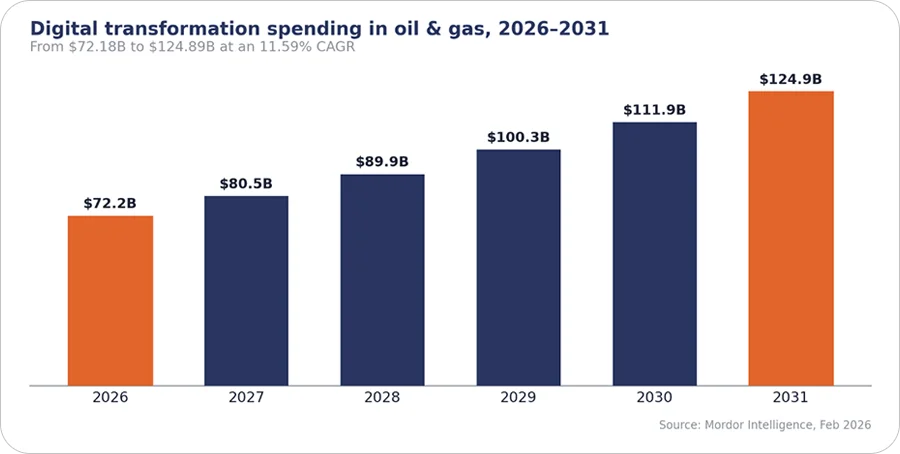

The numbers on digital transformation in oil and gas tell a split story. Spending is climbing fast: the market reached $72.18 billion in 2026 and is on track for $124.89 billion by 2031, an 11.59% CAGR (Mordor Intelligence). Satisfaction has not kept pace. In BCG and DXC's 2025 survey, just 27% of oil, gas, and chemical companies said they were happy with the return on their operational technology and AI investments. Two-thirds of the sector is investing heavily and reporting disappointing returns, and that gap is what makes execution, rather than ambition, the defining question for 2026.

The stall point is well documented: roughly 70% of oil and gas digital transformation initiatives never move beyond the pilot stage (Rystad Energy/DXC). The usual reasons are technical, not strategic. A new platform cannot exchange data with equipment installed twenty years ago, or the data cannot be audited cleanly enough to satisfy a regulator.

Here are the six trends shaping digital transformation in oil and gas in 2026, the engineering each one requires, and the point where projects most often stall.

Spending keeps climbing. Satisfaction with the return does not.

Trend 1: AI & ML for Predictive Operations

The case for AI in oil and gas used to centre on exploration and seismic interpretation. Its scope has widened considerably. AI now operates as a continuous intelligence layer across the asset base, with predictive maintenance the clearest example. Predictive maintenance is the clearest example: instead of servicing equipment on a fixed calendar, operators now predict failures from live sensor data and act before a pump or compressor takes a unit offline.

The numbers behind the shift are hard to argue with:

The harder part of predictive maintenance in oil and gas is rarely the model itself. A model that predicts a bearing failure delivers no value unless the team can retrain and version it, then explain its output after an incident. OT models also age differently from web models. Equipment wears and sensors drift, so a compressor model trained last year quietly loses accuracy unless someone owns the retraining. What actually carries the value is the pipeline around the model: production-grade MLOps built for an OT environment, with the governance and audit trail a turnaround engineer can follow.

This is where the gap between demo and deployment tends to open. A proof of concept that scores well on historical data still has to become a model that runs against live telemetry, holds up under audit, and degrades gracefully when a sensor fails. We build this on stacks like Azure ML and MLflow, and our ML engineering for energy platforms work is mostly about getting models out of notebooks and into the control room without losing the trust that keeps them running.

Trend 2: Digital Twin Deployment at Scale

Digital twins have moved past the demo stage. The market sat at $1.2 billion in 2024 and is forecast to reach $2.81 billion by 2032, an 11.2% CAGR (DataM Intelligence). The growth reflects twins taking on a permanent role in day-to-day operations across the value chain:

BP’s APEX twin and the SLB–Shell deepwater partnership illustrate the working pattern. Each is tied to live telemetry and updated continuously, which keeps it aligned with the physical asset rather than drifting away from it over time.

The integration work is what teams tend to underestimate. A digital twin is only as good as its data feed, so most of the build is real-time integration: IIoT middleware and a simulation layer that sits on top of existing SCADA and historian systems rather than replacing them. The simulation maths is seldom the bottleneck. The difficulty lies in keeping the twin synchronised with physical reality at the latency each use case demands, which ranges from minutes for a reservoir model to sub-second for a safety loop. Teams that handle this well define the data contracts between asset and twin before writing any simulation code.

Trend 3: IT/OT Convergence & IIoT Platform Architecture

Around 70% of oil and gas digital transformation initiatives never leave the pilot stage (Rystad Energy/DXC). The cause is more often technical than strategic or financial. Modern cloud-native platforms have to connect to the legacy operational systems that run the business – SAP, SCADA, and process historians, none of which were built to communicate with a cloud analytics layer.

Where the money actually goes

|

70% |

30% |

Most programmes fail at the integration layer. (Rystad Energy / DXC)

This is an architecture problem, and it has an architecture-led solution. The fix usually involves:

- An API-first integration layer between cloud and OT.

- Edge computing for remote and intermittently connected assets.

- Private 5G readiness and IIoT pipelines that move sensor telemetry from wellhead to cloud without losing fidelity.

- Middleware bridging the IT and OT domains — the component that most often determines whether a pilot reaches production.

This is also where domain experience pays for itself. A historian like OSIsoft PI does not behave like a relational database, and a SCADA protocol was not designed with cloud security in mind. Engineers who have not worked with these systems routinely underestimate the integration effort by an order of magnitude, and that miscalculation is exactly what strands programmes at the pilot line.

Oil and gas companies partnering with Softwarium gain access to distributed engineers specialising in Azure-native cloud architecture, ML engineering, IIoT platform development, and SDET-led quality assurance for mission-critical systems.

Scaling your O&G digital programme?

Trend 4: Cloud-Native Architecture for Field Operations

Cloud deployment in oil and gas is growing at a 13.2% CAGR through 2033, and over 65% of operators have adopted or plan to adopt cloud (Verified Market Reports). The driver is operational rather than cosmetic. Hybrid cloud plus edge delivers real-time field analytics and remote asset management, with capacity that flexes through production peaks instead of requiring upfront investment in on-premise compute that sits underused for most of the year.

The pattern that delivers it: Azure-native cloud architecture for the platform, edge nodes that keep latency-sensitive workloads running at remote sites, and hybrid patterns that let cloud and on-premise operate as one system. A drilling site on a satellite uplink cannot wait for a round trip to a data centre on every decision, so compute has to live at the edge and reconcile with the cloud when the link allows. The aim is to place each workload where its latency and cost profile fit, then engineer for the resilience the field demands.

There is a financial dimension as well, one that concerns the CFO as directly as the CTO. On-premise compute is a capital commitment made years before the real load is known, whereas cloud converts it into an operating cost that tracks usage — valuable in a business where volumes move with the commodity cycle. Predictable workloads stay on owned infrastructure, variable demand bursts to the cloud, and the cost base flexes with the business instead of sitting idle through a downturn. The operators seeing real value treat placement as a deliberate decision: which workloads belong in the cloud, which belong at the edge, and how the two remain consistent when a remote site loses its link for an hour.

Trend 5: ESG Compliance as a Digital Engineering Problem

EU methane rules that took effect in 2025 require quarterly leak detection and repair surveys. That single requirement turned emissions tracking from a spreadsheet job into a continuous-monitoring engineering problem, and it is driving real deployments of IIoT sensors and optical gas imaging. The World Economic Forum estimates full-scale digital adoption could unlock $1.6 trillion in energy-sector value by 2030, with emissions management a meaningful slice of it.

ESG now lives in the data architecture. Meeting it means continuous emissions-monitoring pipelines and carbon-accounting platforms that survive an audit, sometimes backed by digital twins dedicated to methane tracking. The engineering work breaks down to:

- IoT sensor integration across distributed assets.

- Real-time data pipelines feeding the reporting layer.

- Reporting APIs that hand clean figures to disclosure systems.

- Audit-grade provenance, so every reported number traces back to a sensor reading with a timestamp.

Provenance is the part teams skip and regret. A regulator does not just want the emissions figure. They want to know which sensor produced it, when it was last calibrated, and how a raw reading became the reported number. Building that lineage in from day one is far cheaper than reconstructing it under audit. And because the volume of monitoring data is well beyond what any manual process can absorb, the reporting layer is effectively a live system with uptime requirements. Treat ESG as a data-engineering problem and you get a platform you can extend as the rules tighten. Treat it as a yearly scramble and you rebuild it every time they change.

Trend 6: Cybersecurity for OT Environments

94% of the world’s top oil and gas companies had suffered at least one data breach as of 2025 (DXC Technology). As IT and OT converge and more field assets connect to cloud platforms, the attack surface grows with every integration. Ransomware on pipeline systems has already shown what the operational blast radius looks like when an OT environment is compromised.

Security cannot be bolted on after the platform ships. It has to be designed in:

- OT-specific security architecture designed for the control environment.

- Network segmentation that keeps IT and OT domains isolated.

- Zero-trust access for remote field connections.

- Encrypted sensor telemetry and security-by-design baked into IIoT platforms from the first commit.

OT environments also overturn several assumptions carried over from IT. Controls must accommodate availability constraints a corporate IT team rarely encounters. Segmentation, monitoring, and incident response all have to be designed for an environment where uptime is non-negotiable and a forced reboot can trigger a shutdown.

Cybersecurity scales alongside digital transformation rather than as a separate workstream. Each connected sensor, cloud integration, and remote-access path widens the attack surface, so security that suffices for a pilot of a dozen assets will not hold for an enterprise rollout across hundreds of sites. A pilot can omit much of this and still perform convincingly in a demo, but at enterprise scale the same gaps become a serious and quantifiable breach risk.

|

$72.18B O&G digital transformation market, 2026 |

27% satisfied with AI/ML ROI |

94% of top O&G firms breached by 2025 |

Conclusion

Digital transformation in oil and gas does not stall for lack of conviction or budget. What they lack are engineering teams that understand both the technology and the operational reality around it: the SCADA system that cannot go offline, the historian holding thirty years of data nobody wants to migrate. The pilot-to-production gap closes when people who have crossed it before do the work.

Softwarium provides oil and gas software development and IT staff augmentation for the energy sector, building and scaling engineering teams for operators and energy technology vendors.

Sources

- Mordor Intelligence — Digital Transformation Market in Oil & Gas Industry (Feb 2026)

- DXC Technology — Digital Transformation in Oil and Gas: 2026 Outlook (incl. BCG survey data)

- Deloitte Insights — 2026 Oil and Gas Industry Outlook

- DataM Intelligence — Digital Twins in Oil and Gas Market

- Verified Market Reports — Digital Transformation in Oil and Gas Market

- World Economic Forum — Digital adoption value for the energy sector